How does LIFO and FIFO affect financial statements?

By Mia Russell

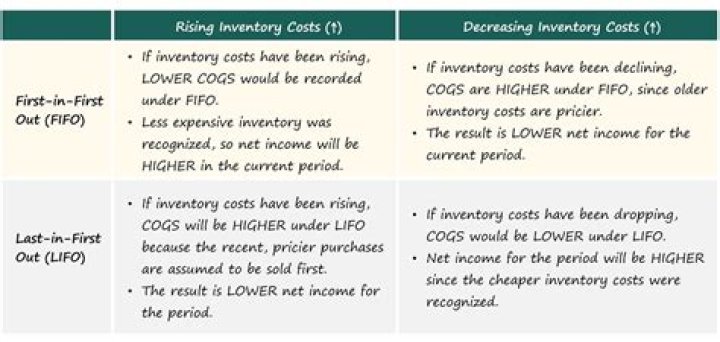

FIFO gives a more accurate value for ending inventory on the balance sheet. On the other hand, FIFO increases net income and increased net income can increase taxes owed. The LIFO method assumes the last item entering inventory is the first sold.

Can you use LIFO for tax purposes and FIFO for financial reporting purposes?

LIFO could be used for U.S. income tax purposes, while FIFO is used for financial reporting.

How LIFO and FIFO affect the cost of goods sold and the valuation of closing stock?

During periods of inflation, the use of LIFO will result in the highest estimate of cost of goods sold among the three approaches, and the lowest net income. This can be used to adjust the beginning and ending inventories, and consequently the cost of goods sold, and to restate income based upon FIFO valuation.

How does LIFO affect net income?

The LIFO valuation method assumes that the last inventory item purchased is the first one used in production or sale. This means that the net income and ending balance amounts are lower under the LIFO method. However, when prices are falling, the LIFO method is likely to generate higher net income.

Why is LIFO not acceptable?

IFRS prohibits LIFO due to potential distortions it may have on a company’s profitability and financial statements. For example, LIFO can understate a company’s earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Can you use LIFO for tax purposes?

A taxpayer electing the Last in – First out (LIFO) method for tax purposes must generally use the LIFO method in its financial statements. For example, a taxpayer may use the double extension LIFO method for financial statement reporting and the link chain LIFO method for income tax reporting.

Which method yields the highest net income?

FIFO

Income effect: FIFO provides the lowest cost of goods sold, the highest gross profit, and the highest net income.

Can a company change from LIFO to FIFO?

Most companies switching from LIFO to FIFO choose to restate their historical financial statements as if the new method had been used all along. It’s important that companies keep precise records to make these changes.

Is LIFO still allowed?

Key Takeaways from Last-in First-Out (LIFO) It provides low-quality balance sheet valuation. It provides high-quality income statement matching. LIFO is prohibited under IFRS and ASPE. However, under the US Generally Accepted Accounting Principles (GAAP), it is permitted.

Which is better for taxes LIFO or FIFO?

The use of LIFO when prices rise results in a lower taxable income because the last inventory purchased had a higher price and results in a larger deduction. Conversely, the use of FIFO when prices increase results in a higher taxable income because the first inventory purchased will have the lowest price.

What method yields the lowest net income?

LIFO

LIFO (Perpetual) In times of rising prices, LIFO (especially LIFO in a periodic system) produces the lowest ending inventory value, the highest cost of goods sold, and the lowest net income.

Does FIFO increase profit?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.