How does Fed rate affect loans?

By John Thompson

For loans, a Fed rate cut could mean lower monthly payments and less interest paid out over the life of the loan. The lower your mortgage rate, the lower your monthly payment and the more home you might be able to afford. Good deal. Note that fixed-rate mortgages are less directly impacted by a Fed rate cut.

What effect does the reserve requirements have on banks ability to lend?

The reserve ratio is the amount of reserves – or cash deposits – that a bank must hold on to and not lend out. The greater the reserve requirement, the less money that a bank can potentially lend – but this excess cash also staves off a banking failure and shores up its balance sheet.

How do a bank’s excess reserves affect how it loans money?

The bank will keep some of it on hand as required reserves, but it will loan the excess reserves out. When that loan is made, it increases the money supply. This is how banks “create” money and increase the money supply. When a bank makes loans out of excess reserves, the money supply increases.

How do interest rates affect bank lending?

Interest rates can change for other reasons and may not change by the same amount as the change in Bank Rate. To cover their costs, banks need to pay less on saving than they make on lending. This means that when Bank Rate comes close to 0%, how far banks pass it on to lower saving and borrowing rates reduces.

Are banks more profitable when interest rates are high or low?

Interest rates and bank profitability are connected, with banks benefiting from higher interest rates. When interest rates are higher, banks make more money, by taking advantage of the difference between the interest banks pay to customers and the interest the bank can earn by investing.

What do low mortgage rates mean for the economy?

Low interest rates reduce mortgage costs, encourage home sales, stabilize or increase home values, and generally push the consumption of goods and services. Normally, this increase in the supply of dollars should decrease their value and increase inflation.

How does a bank’s excess reserves affect money loans?

Excess reserves are a safety buffer of sorts. Financial firms that carry excess reserves have an extra measure of safety in the event of sudden loan loss or significant cash withdrawals by customers. This buffer increases the safety of the banking system, especially in times of economic uncertainty.

How does the reserve requirement impact the ability of banks to make money?

Because banks are only required to keep a fraction of their deposits in reserve and may loan out the rest, banks are able to create money. A lower reserve requirement allows banks to issue more loans and increase the money supply, while a higher reserve requirement does the opposite.

Do banks make loans with excess reserves?

Banks have little incentive to maintain excess reserves because cash earns no return and may even lose value over time due to inflation. Thus, banks normally minimize their excess reserves, lending out the money to clients rather than holding it in their vaults.

How does the Federal Reserve affect interest rates?

The United States Federal Reserve Bank influences interest rates by setting certain rates, stipulating bank reserve requirements, and buying and selling “risk-free” (a term used to indicate that these are among the safest in existence) U.S. Treasury and federal agency securities to affect the deposits that banks hold at the Fed. 4

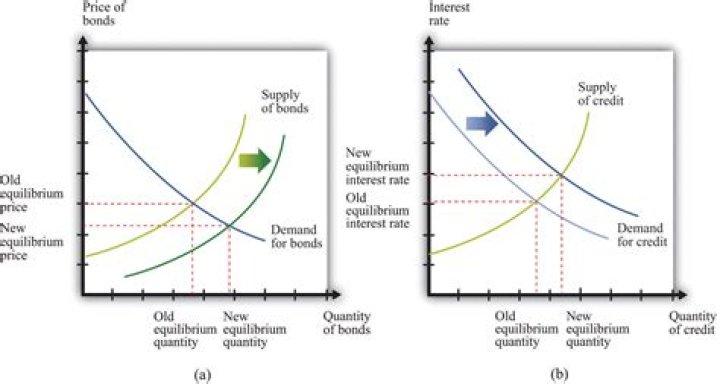

How does a decrease in the reserve ratio affect the money supply?

A decrease in the reserve ratio leads to an increase in the money supply, which puts downward pressure on interest rates and ultimately leads to an increase in nominal GDP. An increase in the reserve ratio leads to a decrease in the money supply, driving interest rates up and pulling nominal GDP downward.

How much money do banks have to have in reserve?

Federal law says that banks must have a reserve that is equal to a certain percentage of the balance in all of their deposit accounts. Any money in their reserve that is more than this percentage is available for lending to other institutions.

Why do banks raise interest rates when demand is low?

Market-Based Factors. When demand is low, such as during an economic recession, banks can increase deposit interest rates to encourage customers to lend, or lower loan rates to incentivize customers to borrow. Local market considerations are also important. Smaller markets may have higher rates due to less competition,…