How do you split a semi variable cost?

By Jessica Hardy

Formula For Semi-Variable Costs

- Semi-variable cost = Fixed cost + variable cost.

- Variable cost per unit = change in cost/change in output.

What is the method used in splitting semi-variable costs to its variable and fixed components?

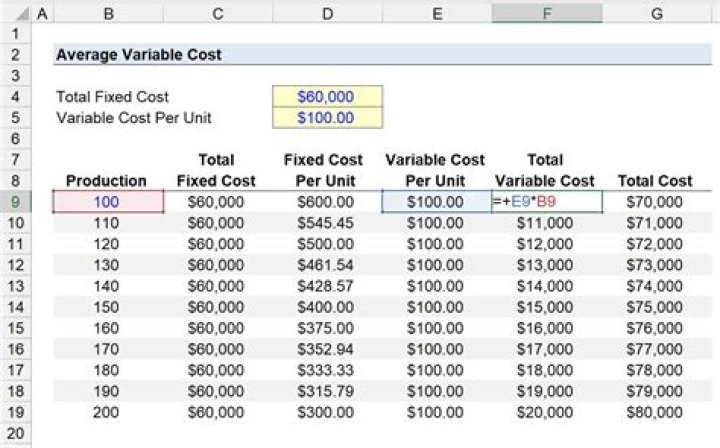

The High-Low method of costing provides a useful cost splitting method. The method is a simple mathematical equation that splits the semi-variable costs into variable and fixed costs. The analysis can also provide useful forecasts for future activity level cost analysis.

Why should semi-variable costs be be segregated into their fixed and variable components?

They vary with production but not in direct proportion to volume. Although semi-variable costs are neither wholly fixed nor wholly variable in nature, they must ultimately be separated into fixed and variable components for the purpose of planning and control.

What is an example of a semi variable cost?

Electricity is a good example of a semi-variable cost. The base rate for service may be constant, but as production grows, power consumption and the company’s electricity bills go up. In other words, there is both a fixed and variable aspect to semi-variable costs.

What is meant by semi variable cost?

A semi-variable cost, also known as a semi-fixed cost or a mixed cost, is a cost composed of a mixture of both fixed and variable components. Costs are fixed for a set level of production or consumption, and become variable after this production level is exceeded.

What is a semi-variable cost examples?

What are cost separation techniques?

I know of three methods for separating mixed costs into their fixed and variable cost components: Prepare a scattergraph by plotting points onto a graph. High-low method. Regression analysis.

What is fixed costs and variable costs?

In accounting, fixed costs are expenses that remain constant for a period of time irrespective of the level of outputs. Variable costs are expenses that change directly and proportionally to the changes in business activity level or volume. Incurred when. Even if the output is nil, fixed costs are incurred.

Why variable costs may be separated from fixed cost?

Being able to separate your fixed costs from your variable costs allows you to calculate a very useful figure; your business’s break-even point. If you sell goods, or if you sell your services priced as units, the break-even point is how many units you need to sell in order to cover all your costs.

What are the 2 types of costs?

The two basic types of costs incurred by businesses are fixed and variable. Fixed costs do not vary with output, while variable costs do. Fixed costs are sometimes called overhead costs. They are incurred whether a firm manufactures 100 widgets or 1,000 widgets.

How semi variable costs or mixed costs can be segregated into fixed and variable components?

2. Scatter-Graph Method: Another approach to the estimation of the fixed and variable components of a mixed cost is the scatter-graph method. The slope of the line is used to estimate the variable costs and the intercept of the line with the vertical axis is considered as the estimated fixed cost.

Why should semi variable costs be be segregated into their fixed and variable components?

How do you separate fixed and variable costs?

What Is the High-Low Method? In cost accounting, the high-low method is a way of attempting to separate out fixed and variable costs given a limited amount of data. The high-low method involves taking the highest level of activity and the lowest level of activity and comparing the total costs at each level.

What are examples of semi variable costs?

Semi-variable costs consist of both fixed and variable costs. Part of the cost stays consistent (often a base cost) and part fluctuates with business activity. Examples include commission payments and overage charges. Commissions are a semi-variable labor costs.

What are examples of semi-variable costs?

What is meant by semi-variable cost?

What are some examples of fixed and variable costs?

What Is the Difference Between Fixed Cost and Variable Cost?

| Fixed Costs | Variable Costs | |

|---|---|---|

| Examples | Depreciation, interest paid on capital, rent, salary, property taxes, insurance premium, etc. | Commission on sales, credit card fees, wages of part-time staff, etc. |

Which is the best method for splitting semi variable costs?

Hi-low is linked to the idea of cost behaviour and is one method for splitting semi-variable costs into their fixed and variable elements. Making a distinction between fixed and variable costs in a semi-variable cost might be used:

How are costs separated into fixed cost and variable cost?

The following methods are used in separation of such costs into fixed cost and variable cost. They are: 1. Industrial Engineering Method 2. Account Inspection Method 3. Scatter Graph Method 4. High and Low Method. 1. Industrial Engineering Method:

How is the variable element of semi variable cost determined?

Under this method, variable and fixed element of semi-variable cost is determined by means of Straight Line Equation, which is as follows: Where, y = Total semi-variable cost m = Variable Cost per unit For January, the equation would be: Rs. 2,000 = 200m+c… (i) and for February, the equation be : Rs. 1.750 = 150m+c … (ii)

Which is the best method to estimate the variable component of a mixed cost?

Another approach to the estimation of the fixed and variable components of a mixed cost is the scatter-graph method.