How are bad debts recorded in financial statements?

By Mia Russell

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Recognizing bad debts leads to an offsetting reduction to accounts receivable on the balance sheet—though businesses retain the right to collect funds should the circumstances change.

How do you write-off a bad debt account?

Under the direct write-off method, bad debts are expensed. The company credits the accounts receivable account on the balance sheet and debits the bad debt expense account on the income statement. Under this form of accounting, there is no “Allowance for Doubtful Accounts” section on the balance sheet.

How do you record uncollectible accounts?

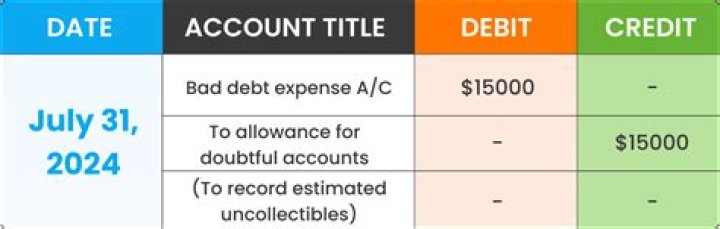

When a specific customer’s account is identified as uncollectible, the journal entry to write off the account is:

- A credit to Accounts Receivable (to remove the amount that will not be collected)

- A debit to Allowance for Doubtful Accounts (to reduce the Allowance balance that was previously established)

What is bad debt for business in one sentence?

Bad debt is a type of debt, which is provided by the company to the creditor or the partner but later on, it becomes non-recoverable. Such that serves as a liability to the company as it does not get paid back by the creditor and possess a loss to the company or the firm.

Is bad debts recorded in profit and loss account?

To Provision for Bad and Doubtful Debts. The Provision for Bad and Doubtful Debts will appear in the Balance Sheet. Next year, the actual amount of bad debts will be debited not to the Profit and Loss Account but to the Provision for Bad and Doubtful Debts Account which will then stand reduced.

Are bad debts liabilities?

So it is considered a liability. But a special type of liability. In other words, doubtful debts or bad debts have already occurred – the debt is bad right now. So you record the loss (expense account) called doubtful debts or bad debts for the amount of $500.

What is bad debts sentence?

A bad debt is a monetary amount owed to a creditor that is unlikely to be paid and, or which the creditor is not willing to take action to collect because of various reasons, often due to the debtor not having the money to pay, for example, due to a company going into liquidation or insolvency.

Where is bad debts shown in final accounts?

The Sundry Debtors appear in the Trial Balance is the net balance after deduction of Bad Debts, during the year. In such case, Bad Debts are debited to Profit and Loss Account and Sundry Debtors, as per Trial Balance, appear in Balance Sheet.

What types of debt should be avoided?

4 Types of Debt to Avoid

- Credit Card Debt. With credit cards promising a luxury and care free lifestyle at the tap of your fingers – it’s no surprise that many people have spiralled into a credit card debt cycle.

- Student Loan Debt.

- Medical Debt.

- Car Loan Debt.

The bad debt expense appears in a line item in the income statement, within the operating expenses section in the lower half of the statement.

What is bad debts in accounting?

Bad debt is an expense that a business incurs once the repayment of credit previously extended to a customer is estimated to be uncollectible and is thus recorded as a charge off.

What will happen if the amount of bad debt expense is understated at year end?

Q 8.23: What will happen if the amount of bad debt expense is understated at year-end? Net income will be understated. Allowance for Doubtful Accounts will be overstated. Net Accounts Receivable will be overstated.

Where is bad debts in balance sheet?

How do you identify uncollectible accounts?

Multiply each percentage by each portion’s dollar amount to calculate the amount of each portion you estimate will be uncollectible. For example, multiply 0.01 by $75,000, 0.02 by $10,000, 0.15 by $7,000, 0.3 by $5,000 and 0.45 by $3,000.

What is the entry for provision for doubtful debts?

Debit provision for bad debts a/c and Credit [profit and loss a/c.

What causes a prior period adjustment in a financial statement?

Since the second situation is both highly specific and rare, a prior period adjustment really applies to just the first item – the correction of an error in the financial statements of a prior period. An error in a financial statement may be caused by: Mistakes in the application of GAAP or some other accounting framework; or

When does an accounting error lead to a prior year adjustment?

If such errors are detected in the current period, then fine, it can be corrected. But often times, these errors are not detected until another accounting year. The correction of these errors in another accounting year, therefore, would lead to prior year adjustment.

What’s the difference between prior year and prior year adjustment?

Prior year adjustment is the correction of prior period errors.

When to present prior year adjustments in IFRS?

Before the 2003 revised IAS 8, the practice has been to present prior year adjustments in the current year statement of comprehensive income.