Can deferred tax asset be current?

By Isabella Wilson

Current Deferred Tax Assets are the current amount a company has overpaid for that can reduce the taxes the company will pay later on. There is some advantage the company will gain in the future. It is an accounting term under the current assets on the company’s finance sheet.

What is deferred tax and current tax?

Current tax is the amount of income taxes payable/recoverable in respect of the current profit/ loss for a period. Deferred tax asset is the income tax amount recoverable in future periods in respect to the deductible temporary differences, carry forward of unused tax losses, and carry forward of unused tax credits.

How do you account for deferred tax assets?

There can be the following scenario of deferred tax asset: If book profit is lesser than taxable profit. Then deferred tax assets get created….Examples of Deferred Tax Asset Journal Entries

- EBITDA = $50,000.

- Depreciation as per books = 30,000/3 = $10,000.

- Profit Before Tax.

- Tax as per books = 40000*30% = $12,000.

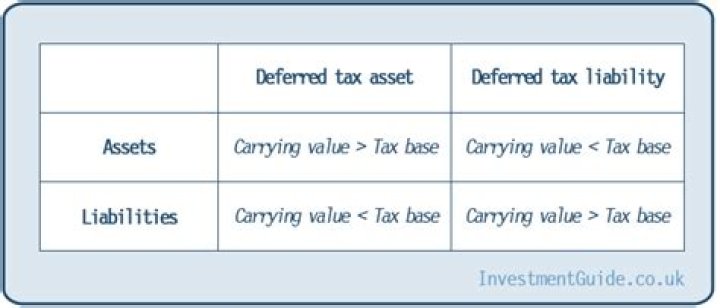

Deferred taxes are a non-current asset for accounting purposes. A current asset is any asset that will provide an economic benefit for or within one year. Deferred taxes are items on the balance sheet that arise from overpayment or advance payment of taxes, resulting in a refund later.

Are capital allowances deferred tax?

In situations where capital allowances exceed the depreciation charged, this will result in a deferred tax liability. The principle behind this is a sound one, as the entity will receive fewer capital allowances in the future, resulting in higher tax charges.

What are current deferred taxes?

Current Deferred Tax Assets are the current amount a company has overpaid for that can reduce the taxes the company will pay later on. It is the opposite of deferred tax liability. It is an accounting term under the current assets on the company’s finance sheet. …

How do I book deferred tax assets?

How is deferred tax calculated on an investment property?

The calculation for the deferred tax liability is: (R75 000 x 28%) + (R100 000 x 28% x 66.6%). The presumption is recovery through sale and therefore, if the building were to be sold at its fair value, the wear and tear allowances to date (R75 000) would be recouped and taxed at 28%.

How is the deferral of capital allowance calculated?

Deferment of Capital Allowance (Section 19) Initial allowance (IA) must be claimed in the YA the capital expenditure was incurred. In the event that IA was not claimed, annual allowance (AA) will be computed based on the full cost, that is, 100% of the cost over the prescribed working life.

Do you have to pay tax on annual investment allowance?

Annual investment allowance. You can deduct the full value of an item that qualifies for annual investment allowance (AIA) from your profits before tax. If you sell the item after claiming AIA you may need to pay tax. You can claim AIA on most plant and machinery up to the AIA amount.

Do you have to defer capital allowance in Ya 2018?

It wishes to defer its claim for capital allowance in YA 2018 as the company is in a loss position. The capital allowance to be deferred is as follows: *The company must defer both the base capital allowance ($5,000) and enhanced capital allowance ($15,000) at the same time.